Perfect 2020 Foresight

Perfect 2020 Foresight

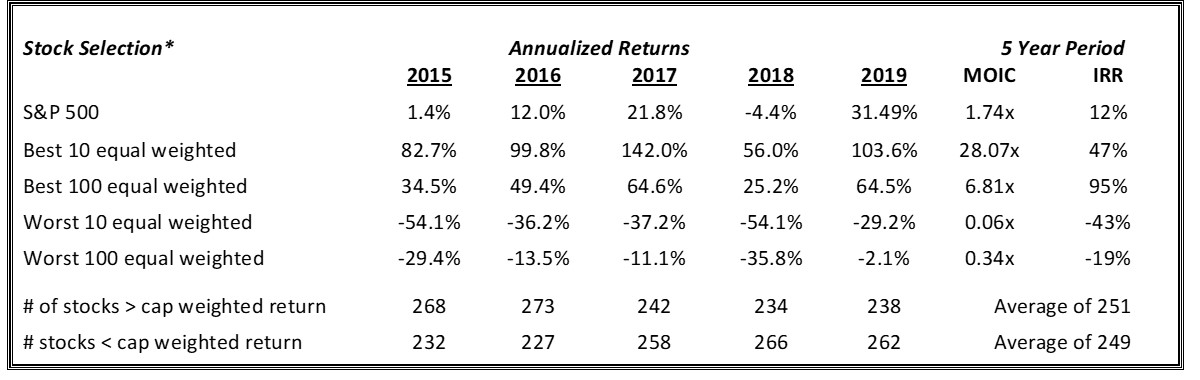

Since it is the year “2020”, I thought it would be fun to look at what investment returns would have been generated by perfectly prescient stock picking over the past five years. What if you had perfect foresight on January 1st each year and created a portfolio of the top stocks for that year?

We know the U.S. equity recovery has been strong and over the past five years the S&P 500 has generated an average annual IRR of 12% on a capital weighted basis, solidly above the long run historical average and helpful in meeting most investors’ goals.

Over the same period, approximately ½ of the stocks in the S&P beat the index return and ½ lagged it on a given year. The number of individual stocks beating the index return ranged from 234 to 273 while the detractors have ranged from 227 to 266 (sometimes the composite stocks change).

But with perfect foresight…

- If you bought the top 100 performing stocks (on an equal weighted basis for the upcoming year) on Jan 1st each year and then rebalanced each Jan 1st, you would have beaten the S&P 500 total return by approximately 35% per annum from 2015 through 2019.

- If you decided to concentrate and picked the top 10 performing stocks each year on Jan 1st, and again rebalanced each year to reflect your foresight, you would have generated a multiple of invested capital of 28.1x over the five-year period – almost 16x better than the index!

- If instead you somehow picked the 100 worst performing stocks each year, and rebalanced annually to magnify your pain, you would have ended the five years with only 34% of your initial capital.

- If you were simply dreadful in an otherwise healthy market, and bought the 10 worst stocks each year, again rebalancing annually, you would have ended up with only 6% of your initial capital.

*The data in this table was generated from the S&P website at www.spindices.com and Refinitiv, www.refinitiv.com. The calculations from this data were performed internally. Perkins deems these sources to be reliable, but they are not in any way guaranteed and should not be considered as any form of an investment recommendation.

Best wishes to all of you seeking alpha in 2020. May the foresight be with you!

_____________________

Douglas Newsome, CFA

Managing Director, Director of Research

Perkins Fund Marketing