Vivamus quis sapien cura

10 YEARS OF EXCELLENCE

Phasellus nec dolor.Sed ornare semper ipsum. Sed pede orci volutpat sed congue vels gravida non lacus.Vivamus quis sed metus quisque gravida Quisque blandit sem esed erat. Maecenas porttitor neque eu sem. Nullam lectus neque, blandit quis mattis quis varius eu eros. Vivamus ads metus. Mauris at tellus at sapien.

OUR MOST ADVANTAGES

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

HENRIETTA WEB

Web Developer

LEO MULLINS

Founder, CEO

STEVE HARPER

Developer

JANINE STYLES

Developer

MARGARET HUDSON

Lead Designer

Quo ad clita prompta, has causae dolorem commune ex, possim habem definitiones. Tota corrumpit voluptatum pri id, dicta quando deleniti vel an, id simul consectetuer mea. Ad vidisse facilis sit, te dolore signiferumque nam.

Quo ad clita prompta, has causae dolorem commune ex, possim habem definitiones. Tota corrumpit voluptatum pri id, dicta quando deleniti vel an, id simul consectetuer mea. Ad vidisse facilis sit, te dolore signiferumque nam.

Quo ad clita prompta, has causae dolorem commune ex, possim habem definitiones. Tota corrumpit voluptatum pri id, dicta quando deleniti vel an, id simul consectetuer mea. Ad vidisse facilis sit, te dolore signiferumque nam.

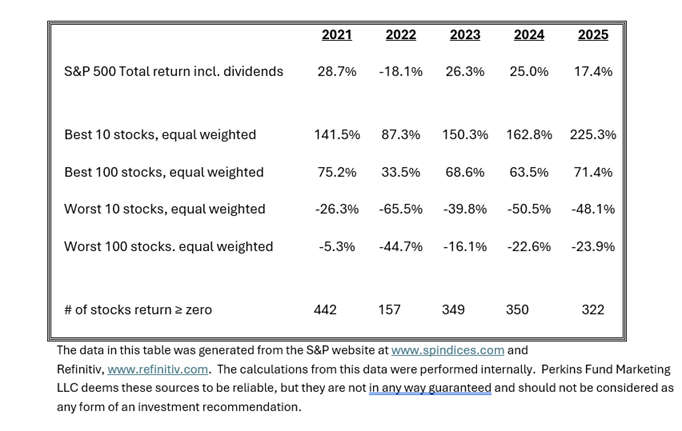

2025 S&P 500 Perfect Hindsight

On the flip side, not every stock that joined the S&P 500 did well. Trade Desk shares were the worst performers in the index with a 67.7% loss, while Block dropped 23.4% and Coinbase gave up 8.9%.

The equal-weighted S&P 500 underperformed the cap weighted index by 6.45%, continuing the trend for the past 22 years! Let that sink in! The13 years prior the equal-weighted in index routinely beat the cap weighted index.

- If you bought the top 100 performing stocks in the S&P 500 on an equal-weighted basis on Jan 2nd, 2025, and held them throughout the year, you would have been up an outstanding 71.4% and crushed the S&P 500 total return by over 54%.

- If you concentrated and picked the top 10 performing stocks on Jan 2nd, and again held them all year, you would have generated an amazing total return of 225.3%, a much higher top ten outperformance and very indicative of the market concentration in 2025.

- If you picked the 100 worst performing stocks for the year, you would have to mark your portfolio down 23.9%.

- If you only owned the worst 10 S&P 500 stocks for the year, you would have finished the period down a miserable 48.1% (and a massive differential to the top 10 performers).

For 2025, the S&P was positive 8 out of 12 months amid news headlines that included: tariff gyrations, AI FOMO including datacenters, crypto sagging while gold surged (Newmont up 170%), and interest rates were cut with possibly more to come in 2026.

Don’t be shy. We would love to hear from you.

Best wishes to all for a happy, healthy and prosperous 2026!

J. Douglas Newsome, CFA

Managing Director, Director of Research

Perkins Fund Marketing LLC

2024 S&P 500 Perfect Hindsight

- If you bought the top 100 performing stocks in the S&P 500 on an equal weighted basis on Jan 2nd last year and held them through the year, you would have been up 63.5%, beaten the S&P 500 total return by almost 40% as well as the “magnificent seven” by over 21%.

- If you concentrated and picked the top 10 performing stocks on Jan 2nd, and again held them all year, you would have generated a total return of 162.8%, the most lopsided performance for the top 10 stocks in many years.

- 10 of the 11 S&P industry sectors were positive, expanding breadth from 2023 and a huge turnaround from 2022 when 10 of 11 were negative. Energy generated the third worst sector returns in 2023 following the second worst sector returns in 2023 (and best in 2022).

- If you picked the 100 worst performing stocks for the year, you would have to mark your portfolio down 22.6% (tough but nothing like 2022).

- If you only owned the worst 10 S&P 500 stocks for the year, you would have finished the year down 50.5% (marginally better than 2018 and 2015 but still brutal).

In 2024, the growth stock train stayed on track, and interest in artificial intelligence continued unabated.

Presidential election influence on the stock market is a hot topic on the financial stations. What we do know is that in the fourth year of a president’s term, the market has been up in 21 of the last 25 elections. Past performance, however, is no guarantee of future returns - including election years.

We would love to hear from you.

Best wishes to all for a happy, healthy and prosperous 2024!

J. Douglas Newsome, CFA

Managing Director, Director of Research

Perkins Fund Marketing LLC

2023 S&P 500 Hindsight

- If you bought the top 100 performing stocks in the S&P 500 on an equal weighted basis on Jan 2nd last year and held them through the year, you would have been up 68.6%, and beaten the S&P 500 total return by over 40%.

- If you concentrated and picked the top 10 performing stocks on Jan 2nd, and again held them all year, you would have generated a total return of 150.3%, and demolished the “magnificent seven” by more than 80%.

- 8 of the 11 S&P industry sectors were positive, a huge turnaround from 2022 when 10 of 11 were negative. Last year’s hero, energy, generated the second worst sector returns in 2023.

- If you picked the 100 worst performing stocks for the year, you would have to mark your portfolio down 16.1%.

- If you only owned the worst 10 S&P 500 stocks for the year, you would have finished the year down 39.8%.

In 2023, the growth stock train got back on track, in particular anything to do with artificial intelligence.

2024? Do presidential elections influence the stock market? On the one hand, in the fourth year of a president’s term, the market has been up in 20 of the last 24. On the other, you can't always count on future returns to match past ones. Despite some consistent patterns, election years are no exception.

We would love to hear from you.

Best wishes to all for a happy, healthy and prosperous 2024!

J. Douglas Newsome, CFA

Managing Director, Director of Research

Perkins Fund Marketing LLC

Conference Strategy Best Practices 2024

Here are some best practices to follow to generate the most ROI from your meetings with investors.

Preparation:

- Know your investor: Conferences typically provide some limited background as a start. Bolster this information with a review of LinkedIn and any investor databases you may have access to. Do not forget mutual contacts and any common interests, background, etc.

- Save the trees: Investors are taking 15 or more meetings. They do not want to bring back 15+ presentation decks. Bring a one-pager and possibly a few exhibits to add color to the conversation - but not to hand out.

- Practice your pitch: a 30-minute meeting is really an 8-10 minute, concise introduction to your strategy. You will have a few minutes to allow the investor to speak at the beginning and time after to ask questions.

- Divide the pitch: The presentation should be made in chapters including: team (people), philosophy/opportunity, process, portfolio, performance and risk management. You must also be sure to tell the investor how they can invest – on or off-shore, minimum size, etc. as well as how they can (or cannot) redeem.

The “Big” Event:

- Why are you there? Introduce your fund and strategy and start a relationship. Period.

- Make it repeatable. If your investor cannot repeat three points about you, your fund will get lost in the shuffle. Remember that investors will conduct 15+ meetings and they will only remember 5-6 of them.Focus on what you want the investor to know about you and then what you want them to remember.Why this strategy/opportunity? Why us? and Why Now?

8 Do’s:

- Take notes on all the questions asked and your follow-up’s

- Offer a coffee or water or snack for the investor and have mints at the table

- Have physical tear sheets and QR code tear sheets available

- Be enthusiastic – if you don’t care, the investor won’t care

- Ask the investor questions during the meeting to better understand their concerns and interests

- Ask for a “60-second” intro from the investor (unless you know them well)

- Ask the investor how much they know about or their experience they have with the asset class or strategy

- At the conclusion of the meeting ask about the best way/time to follow-up

5 Do Not’s:

- Read from slides

- Speak fast or in vague terms

- Interrupt or cut off investor questions or comments

- Avoid answering challenging questions

- Keep the investor past the meeting end time (unless they ask)

Follow-up:

- Send a thank you follow-up note that references the meeting and any follow-up questions that came about. Do this within days of the event.

- Add the investors to the distribution list for performance and other updates.

- Take every opportunity to share your expertise and educate the investor on developments in your market / asset class with regular insights.

- Ask the investor for feedback. Do not hesitate to ask what the investor’s initial thoughts are on both the strategy and the approach. The investor may have enjoyed the meeting but has zero budget or plans to invest.

Don’t forget to practice.

Happy hunting!

Best regards,

J. Douglas Newsome, CFA

Managing Director, Director of Research

Perkins Fund Marketing LLC

2022 S&P 500 Hindsight

2022 was a lost year for most long only strategies with notable and significant sector and geographic exceptions. Hedge funds overall generated alpha and a good number posted very good returns. Violent swings and a wide dispersion of returns was once again the norm. The total market value of the S&P was $40.36 trillion to begin 2022 and finished the year at $32.13 trillion.

- If you bought the top 100 performing stocks in the S&P 500 on an equal weighted basis on Jan 1st last year and held them through the year, you would have been up 33.5%, and beaten the S&P 500 total return by over 50%.

- If you concentrated and picked the top 10 performing stocks on Jan 1st, and again held them all year, you would have generated a total return of 87.3%, more than 100% greater than the S&P.

- 10 of the 11 S&P industry sectors were negative. However, if you had gone all-in on energy stocks, the S&P 500 Energy Sector Index .SPNY generated a 59% return.

- If instead you picked the 100 worst performing stocks for the year, you would have to mark your portfolio down 44.7%.

- If you were in the worst 10 S&P 500 stocks for the year, you would have finished the year down 65.5%. To contrast, Bitcoin (BTC) lost 65.2% in 2022.

The data in this table was generated from the S&P website at www.spindices.com and Refinitiv, www.refinitiv.com. The calculations from this data were performed internally. Perkins Fund Marketing LLC deems these sources to be reliable, but they are not in any way guaranteed and should not be considered as any form of an investment recommendation.

In 2022, investors who had ridden the growth stock train got derailed. Old fashioned value stock pickers got some revenge and the energy sector had a huge year.

2023 is off to a promising start. As always, we welcome the opportunity to speak with you.

Best wishes to all.

J. Douglas Newsome, CFA

Managing Director, Director of Research

Perkins Fund Marketing LLC

What is “Institutional Quality”?

From single family offices on up through to large public pension plans and even sovereign wealth funds, investors (allocators) are much more likely to engage with investment managers who have some degree of institutional pedigree, polish, credibility, and professionalism. Investors do this as a way to “de-risk” their initial investment allocation and to make the process of tracking the investment more manageable. Since it is not always clear to those raising capital what it means to have an “institutional quality”, we thought it would be helpful to list a few key elements.

The following are Ten Signs of institutional quality that investors actively or subconsciously look for in an investment manager:

- Firm leaders are well-spoken, dress appropriately, responsive and clear in their messaging. Meetings and calls are interactive, properly paced, and respectful.

- The manager can comfortably field tough questions and does not display angst discussing their investment process, philosophy, team, and challenging periods in their track record.

- The manager’s investment strategy is described in a concise fashion such that the allocator can repeat it to his/her colleagues.

- Follow-up after calls and meetings from the placement agent and/or manager are gently persistent, informational, and help to develop a relationship.

- An institutional quality manager will deliver performance that meets or exceeds expectations and when they do not, the manager is transparent as to the reasoning and steps to correct going forward.

- Certain strategies lend themselves to a need for NDAs. The manager must be comfortable sharing enough information so that a potential investor can determine whether they even want to go through the NDA process.

- Following all steps from initial call/email through to signing subscription docs, the manager is one step ahead and is in a position to provide a teaser, a presentation deck, performance attribution, data room, any/all docs, etc.

- Marketing materials must be polished, professional, error free, and cannot contain unserious, amateurish graphics.

- The senior team members have experience, relevant track records, and well-written bios.

- Senior team members must be polite, kind, and pleasant to work with and should not shy away from being direct and candid. During due diligence and negotiations, the senior firm members must not get too heated or impulsive.